Cross-Border E-Commerce

US & Canada Sales Tax Playbook

A practical guide to US Wayfair economic nexus and the Canada GST/HST/PST framework — the compliance roadmap for Amazon FBA, Shopify, and cross-border sellers.

Canada Sales Tax

Why Cross-Border Sellers Must Understand Canadian Sales Tax

Many ecommerce sellers assume Amazon handles everything. In reality, Canada's sales tax system is a dual federal + provincial architecture with widely varying rules by province. Sellers may trigger registration obligations due to inventory storage, sales thresholds, or sales through their own website — even if they only sell through marketplace platforms.

- 01 Five Tax Types — Federal GST 5% · HST 13–15% · Provincial PST/RST · Quebec QST · Manitoba RST

- 02 MPF Collection — Since 2021, Amazon.ca auto-collects in all provinces, but seller registration obligations remain

- 03 Thresholds — GST/HST small supplier exemption is CAD $30,000; non-resident sellers face separate registration rules

Four Key Sales Tax Types in Canada

Canada Provincial Sales Tax Rate Table (2026)

| Province / Territory | Tax Type | GST | Provincial | Total | Amazon Collects |

|---|---|---|---|---|---|

| Ontario ON | HST | — | — | 13% | ✓ Yes |

| Quebec QC | GST+QST | 5% | 9.975% | 14.975% | ✓ Yes |

| British Columbia BC | GST+PST | 5% | 7% | 12% | ✓ Yes |

| Alberta AB | GST | 5% | — | 5% | ✓ Yes |

| Manitoba MB | GST+RST | 5% | 7% | 12% | ✓ Yes |

| Saskatchewan SK | GST+PST | 5% | 6% | 11% | ✓ Yes |

| New Brunswick NB | HST | — | — | 15% | ✓ Yes |

| Nova Scotia NS | HST | — | — | 14% | ✓ Yes |

| Prince Edward Island PE | HST | — | — | 15% | ✓ Yes |

| Newfoundland & Labrador NL | HST | — | — | 15% | ✓ Yes |

| Yukon / NWT / Nunavut | GST | 5% | — | 5% | ✓ Yes |

⚠️ Amazon collects tax as an MPF, but sellers must still confirm their registration status and file periodic returns.

Non-Resident Registration Thresholds

Registration Decision Flow

Canada 5-Step Compliance Roadmap

US Sales Tax

Post-Wayfair · Economic Nexus in 45 States

Following the 2018 South Dakota v. Wayfair Supreme Court decision, all 45 sales-tax states adopted economic nexus rules — meaning remote sellers must collect and remit sales tax once sales thresholds are crossed, even without physical presence. Amazon FBA inventory creates immediate physical nexus; Shopify independent stores are entirely the seller's responsibility.

Key State Thresholds (2026)

| State | Sales Threshold | State Rate | Amazon | Notes |

|---|---|---|---|---|

| California CA | $500,000 | 7.25% | ✓ | Local tax up to 10% |

| Texas TX | $500,000 | 6.25% | ✓ | Separate Permit required |

| New York NY | $500K & 100 transactions | 4.0% | ✓ | State+city can reach 8.875% |

| Florida FL | $100,000 | 6.0% | ✓ | FBA warehouse = physical nexus |

| Washington WA | $100,000 | 6.5% | ✓ | Also has B&O business tax |

| Illinois IL | $100,000 | 6.25% | ✓ | Combined rate can reach 11% |

| Pennsylvania PA | $100,000 | 6.0% | ✓ | Common FBA warehouse state |

| Alabama AL | $250,000 | 4.0% | ✓ | Higher threshold state |

| Most Other States | $100,000 | 4–7% | ✓ | DE/MT/NH/OR: no sales tax |

Sources: Avalara / Tax Foundation (updated April 2026) · Verify with each state's official website

Amazon vs. Shopify — Sales Tax Mechanics Compared

Amazon · Platform Collection

- Amazon auto-collects and remits sales tax in all sales-tax states as an MPF

- FBA distributes inventory to multiple state warehouses — creating physical nexus even at low sales volumes

- Platform collection ≠ state income tax filing; you must still assess state income/franchise tax obligations

- Sales of $5,000+ generate a 1099-K that state tax agencies cross-reference

Shopify · Seller's Responsibility

- Shopify independent stores are NOT Marketplace Facilitators — full tax obligation rests with the seller

- Since 2025, orders via the Shop App are collected by Shopify; orders via your own domain remain your responsibility

- Enable tax rates state-by-state in Settings → Taxes and enter each Permit number

- File monthly/quarterly even with zero sales — zero-dollar filings are required in most states

All-State Economic Nexus Thresholds (2026)

All 50 states' economic nexus thresholds · Source: Avalara / Tax Foundation (2026)

| State | Abbr. | Effective Date | Sales Threshold | Transaction Count | Marketplace | Reporting |

|---|---|---|---|---|---|---|

| Alabama | AL | 10/1/2018 | 250000 | na | Excluded | |

| Alaska | AK | 100000 | Included | |||

| Arizona | AZ | 2019-10-01 | 100000 | Excluded | ||

| Arkansas | AR | 2019-07-01 | 100000 | 200 | Excluded | |

| California | CA | 2019-04-01 | 500000 | Included | ||

| Colorado | CO | 2019-04-14 | 100000 | Excluded | ||

| Connecticut | CT | 12/1/2018 | 100000 | 200 | Included | |

| D.C. | DC | 2019-01-01 | 100000 | 200 | Included | |

| Florida | FL | 2021-07-01 | 100000 | Excluded | ||

| Georgia | GA | 2020-01-01 | 100000 | 200 | Excluded | |

| Hawaii | HI | 7/1/2018 | 100000 | 200 | Included | |

| Idaho | ID | 2019-06-01 | 100000 | Included | ||

| Illinois | IL | 10/1/2018 | 100000 | 200 | Excluded | |

| Indiana | IN | 10/1/2018 | 100000 | Excluded | ||

| Iowa | IA | 1/1/2019 | 100000 | Included | ||

| Kansas | KS | 2021-07-01 | 100000 | Included | ||

| Kentucky | KY | 10/1/2018 | 100000 | 200 | Included | |

| Louisiana | LA | 2020-07-01 | 100000 | Excluded | ||

| Maine | ME | 7/1/2018 | 100000 | Excluded | ||

| Maryland | MD | 10/1/2018 | 100000 | 200 | Included | |

| Massachusetts | MA | 2019-10-01 | 100000 | Excluded | ||

| Michigan | MI | 10/1/2018 | 100000 | 200 | Included | |

| Minnesota | MN | 2019-10-01 | 100000 | 200 | Included | |

| Mississippi | MS | 9/1/2018 | 250000 | Excluded | ||

| Missouri | MO | 2023-01-01 | 100000 | Included | ||

| Nebraska | NE | 2019-04-01 | 100000 | 200 | Included | |

| Nevada | NV | 2018-11-01 | 100000 | 200 | Included | |

| New Jersey | NJ | 2018-11-01 | 100000 | 200 | Included | |

| New Mexico | NM | 2019-07-01 | 100000 | Excluded | ||

| New York | NY | 2018-06-24 | 500000 | 100 | Included | |

| North Carolina | NC | 11/1/2018 | 100000 | Included | ||

| North Dakota | ND | 10/1/2018 | 100000 | Excluded | ||

| Ohio | OH | 2019-08-01 | 100000 | 200 | Included | |

| Oklahoma | OK | 2019-11-01 | 100000 | Excluded | ||

| Pennsylvania | PA | 2019-07-01 | 100000 | Included | 10000 | |

| Rhode Island | RI | 8/17/2017 | 100000 | 200 | Included | |

| South Carolina | SC | 11/01/2018 | 100000 | Included | ||

| South Dakota | SD | 11/1/2018 | 100000 | Included | ||

| Tennessee | TN | 2019-10-01 | 100000 | Excluded | ||

| Texas | TX | 2019-10-01 | 500000 | Included | ||

| Utah | UT | 1/1/2019 | 100000 | Excluded | ||

| Vermont | VT | 7/1/2018 | 100000 | 200 | Included | |

| Virginia | VA | 2019-07-01 | 100000 | 200 | Excluded | |

| Washington | WA | 2019-03-14 | 100000 | Included | 10000 | |

| West Virginia | WV | 2019-01-01 | 100000 | 200 | Included | |

| Wisconsin | WI | 10/1/2018 | 100000 | Included | ||

| Wyoming | WY | 2019-02-01 | 100000 | Excluded | ||

| Note 1: Reporting requirement: Generally speaking, if a seller does not collect sales/use taxes, there is a reporting requirment for the seller to report name of customer, address, order date and amount etc. | ||||||

| Other than economic nexus, sellers or other businesses with inventories, sales person, servers to receive orders or other factors which may create sales/use tax nexus in a state should consult a professional accountant or tax adviser to ensure sales/use tax compliance. For most states, keeping inventories in a warehouse in a state creates sales/tax nexus. Therefore, FBA sellers likely have sales/use tax nexus in any FBA state where they have inventories. |

🗺️ Interactive US Sales Tax Maps

US Economic Nexus Threshold Map

Displays threshold type by state — sales-only / sales or transactions / no state sales tax. Hover to see details.

Do Exempt Sales Count Toward Nexus? (By State)

Shows whether each state counts exempt sales toward the economic nexus threshold — a key compliance distinction.

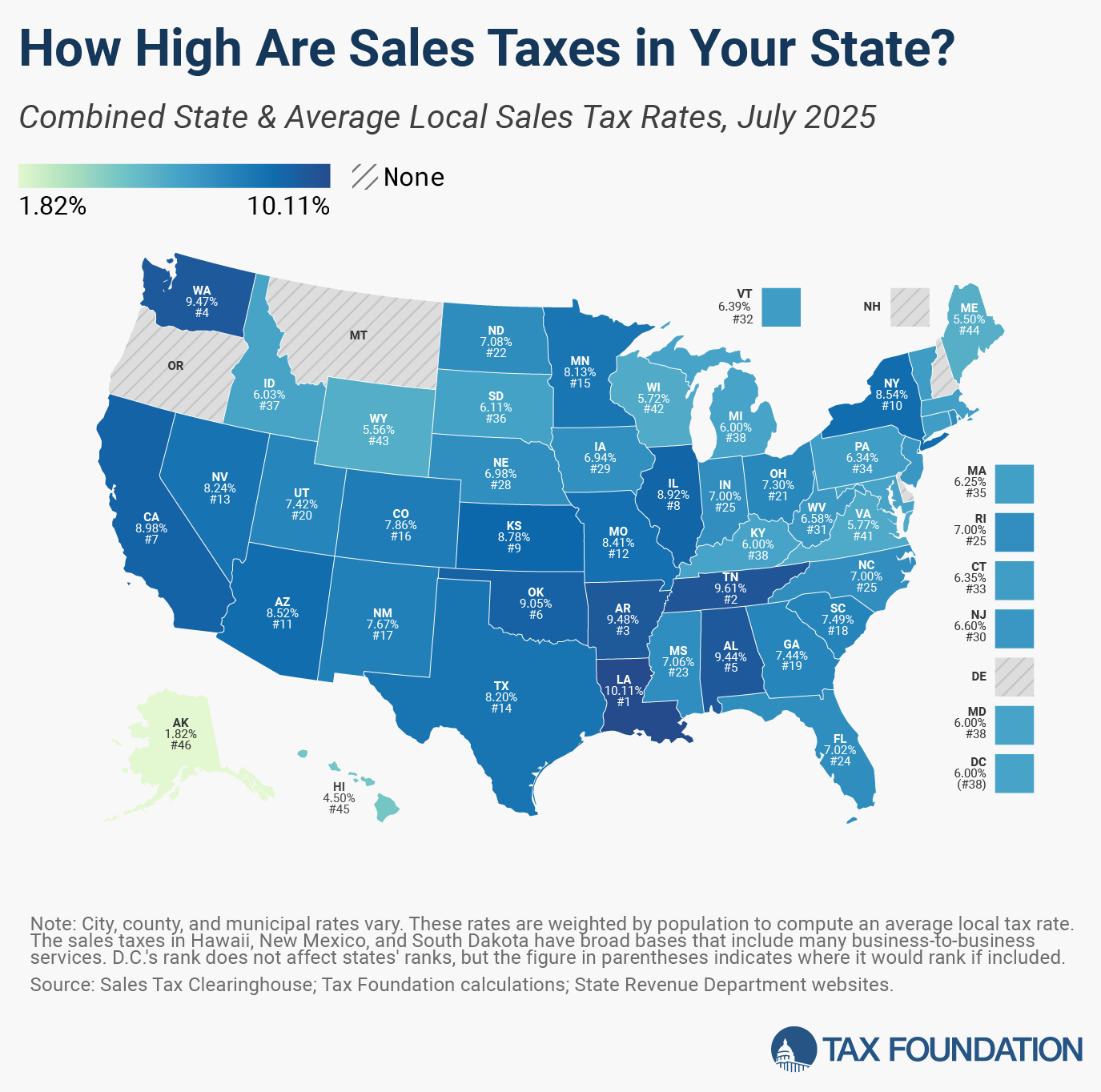

Combined State & Average Local Sales Tax Rate Map

Visual overview of each state's total tax burden — combined state-level and average local sales tax rates.

US 5-Step Compliance Roadmap

Frequently Asked Questions

🇺🇸 US Sales Tax

🇨🇦 Canada Sales Tax

Disclaimer: This content is updated as of 2026 and is for general informational purposes only. It does not constitute professional tax, legal, or accounting advice. Please consult a licensed professional for guidance specific to your situation.

Still have questions after reading?

Book a free 30-minute assessment with a US & Canadian CPA — tailored to your specific situation.

Book Free Assessment